Employers’ Guide

Download your guide to doing business with us. Find everything you need to know about employees, employers and self-employed persons registration, monthly contribution rates, taxable and non-taxable earnings/allowances, business notices and our annual compliance audit.

Click here to download your copy.

Employers Remittance (R3A) Forms

Instantly access your contribution forms with our direct download link. Click here.

Email your signed PDF R3A file to contributions@mbs.gov.ag. Photographs of your R3A forms are not permitted.

Click here for more MBS forms.

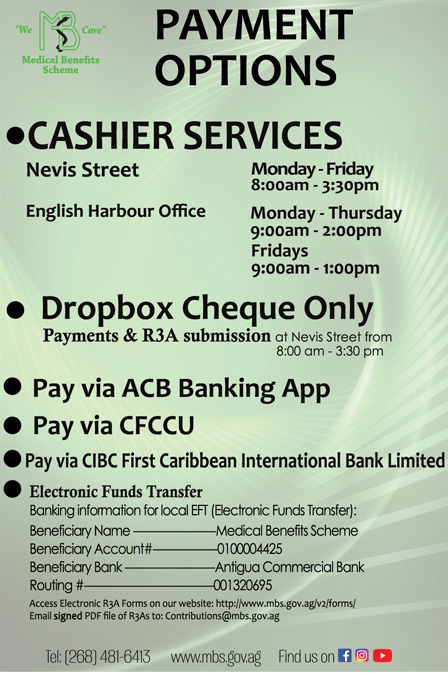

Contribution Payment Options

Submit your MBS contributions using any of the following payment options:

Testimonials

Hear stories from our beneficiaries overcoming their health challenges through treatment and health education.

How to make an appointment online to renew your MBS card

Is your MBS card expired? Making an appointment to renew is easy! Here’s how

MBS News Update

Connect with us through our MBS News Update.

Watch our latest informative show focused on health and wellness topics, our services offerings and policies and keep updated on your benefits.

MBS Smartcard Replacement Policy

How to replace your lost/stolen card

How does someone register as a beneficiary at the Medical Benefits Scheme?

Visit our Registration Department on Nevis Street, to become a registered beneficiary of the Scheme.

The required documents needed to register are:

Nationals

- Valid Passport or, Birth certificate and a valid government-issued photo ID.

- Social Security Card

Registering children who were born within Antigua & Barbuda.

The child must be accompanied by a parent with the following documents:

- Birth paper

- Passport

- Parent’s passport

Non-National

- Valid Passport

- Social Security Card

Registering children who were not born within Antigua & Barbuda.

The child must be accompanied by a parent with the following documents:

- Birth certificate

- Passport

- Letter from the school they attend

- Parents passport

NB. Non- Notional applicants, must be legally residing in Antigua & Barbuda for twelve (12) consecutive months before they can be registered into the scheme.

For further information on the registration process, call us 481-6369/6371

How do I become eligible for benefits?

Registered members are required to make a minimum of six (6) months contributions, to become eligible to claim benefits from the scheme. Once the required amount of contributions has been made, the beneficiary would then be issued a smartcard, that the individual can use to make claims, fill prescriptions at any of our six (6) satellite pharmacies, as well as when they visit the Mount St. John’s Medical Center.

Membership has its privileges!

What benefits can I claim from MBS?

The Medical Benefits Scheme covers eleven (11) diseases beneficiaries can make claims for reimbursement from Doctor’s visits, but only for the listed illnesses that is covered by the Scheme. Click here for a list of the covered diseases.

Beneficiaries can also make claims for lab tests, surgeries and other medical procedures (such as X-rays, ultrasounds etc.) which have been performed within their doctor’s private office. We also accept claims for overseas medical treatment. Click here to learn more about making claims.

Does my contribution to the Medical Benefits Scheme cover my spouse and/or child?

No, your contributions would not cover your spouse or child, because each beneficiary is entitled to hold his/her own card. That being said, they can be registered as members of MBS.

See requirements on being registered.

I am currently unemployed. What can I do to keep my benefits active?

Persons between the ages of 16 – 69, who are unemployed for 3 months or more, can register as a voluntary contributor, to make payments to MBS. Making regular contributions, allows the beneficiary to continue receiving benefits from the scheme.

To learn more about this process, call or visit our Registration Department, on Nevis Street at 481-6369/6371.